Tax-Efficient Retirement Planning in Minnesota: A Guide for Near-Retirees

Key Takeaways:

- Minnesota taxes most retirement income, including IRAs, 401(k)s, and even Social Security for many residents, making tax planning important for preserving wealth.

- Strategies like Roth conversions, Qualified Charitable Distributions (QCDs), and diversified withdrawal sequencing can significantly reduce your long-term tax burden.

- Minnesota’s unique estate tax and lower exemption thresholds require careful legacy planning to avoid unnecessary taxes and protect your heirs.

As retirement approaches, many people focus on investment returns, lifestyle goals, and income planning. However, one piece that often doesn’t get enough attention is tax efficiency. The way your income is structured in retirement can have a significant impact on how long your savings last and how much flexibility you have with your money. Here in Minnesota, the tax environment adds another layer of complexity, with state income taxes applying to most types of retirement income, including Social Security, for many residents. That means a tax-smart approach isn’t just a nice-to-have; it’s also important for protecting your nest egg. In this post, we’ll explore practical strategies designed to help near-retirees keep more of what they’ve worked hard to save, while navigating both federal and Minnesota-specific tax rules.

Understanding Minnesota’s Tax Landscape for Retirees

Minnesota has a graduated state income tax with tax rates ranging from 5.35% to 9.85%. Similar to the federal income tax system, your first layer of income is taxed at a lower rate and then at progressively higher rates for higher income brackets. Minnesota’s top tax rate, 9.85%, ranks in the top ten for all states, making us a relatively high tax state.

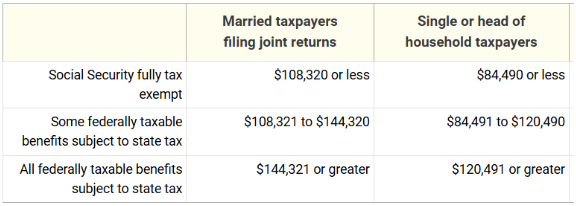

Minnesota does tax most forms of income, which includes various retirement income sources. All pensions and withdrawals from retirement accounts, such as 401ks and IRAs, are generally subject to state-level taxation. The state passed somewhat recent legislation in 2023 that does provide an enhanced subtraction of Social Security benefits for residents with income below a certain threshold. Those who have adjusted gross income (AGI) below $108,320 (married filing jointly) and $84,490 (single) will be totally exempt from paying state taxes on their Social Security benefits. As AGI increases, the exemption phases out until reaching $144,321 (married filing jointly) or $120,491 (single). For more on the specifics, check out our blog post on the subject.

Minnesota residents are also subject to property taxes through their county and a sales tax on goods and services at a rate of 6.875%. There are several categories of goods exempt from the sales tax, including food, clothing, home heating fuels, all drugs for human consumption, newspapers, and magazines.

How Retirement Accounts Are Taxed in Minnesota

If you are approaching retirement, then you have likely accumulated value in a traditional 401k plan or IRA. You contributed these funds before you paid taxes on them, so when it comes time to take the money out, the value will be fully taxed just like your paycheck (also known as ordinary income). This is true both for federal and state taxes, as Minnesota conforms to federal tax law on this matter.

Both traditional pre-tax 401ks and IRAs will eventually require you to withdraw money from the account, even if you don’t need the funds. These distributions are known as Required Minimum Distributions (RMDs) and must start at your required beginning date (age 73 currently, changing to 75 in 2033). As you can imagine, these RMDs can often be large after accumulating lots of value in your 401k plan over many years. This can lead to a large tax hit when it comes time to take the money out.

Two strategies that may help to reduce your RMD tax hit are:

- Roth Conversions - Roth IRAs consist of after-tax contributions that grow and can be distributed tax-free if you follow the rules. Not only are distributions tax-free, but there are no RMDs for the owner. Although you will pay taxes on the conversion, you are allowed to convert pre-tax IRA money into Roth IRA money. These conversions can help to lower your RMD by reducing your traditional IRA value and increasing your Roth IRA value.

- Charitable giving - You are allowed to give money directly to a charity out of your traditional IRA without paying any taxes on the donation. These donations are known as Qualified Charitable Distributions (QCDs) and can be a very useful tool for those who do not need their entire RMD and would like to reduce their taxable income.

You can read more on what to do if you will not need your RMD in a past blog post.

Strategies for Tax-Efficient Withdrawals

One key to reducing your tax bill in retirement is to consider strategies that will maximize the tax efficiency of your retirement income sources. Many folks approach retirement with money in only one type of account, most often a traditional pre-tax 401 (k) or IRA. It can be very helpful to consider diversifying by account type as you accumulate for retirement and contribute funds to taxable brokerage accounts, Roth IRAs, or 401 (k) s and/or Health Savings Accounts as you are able.

To help increase account diversification and make tax-efficient use of accounts, consider the following strategies:

- Sequencing Withdrawals – Deciding whether to draw from taxable, tax-deferred, or Roth accounts first can help smooth income over time and keep you in lower tax brackets. By balancing withdrawals strategically, retirees can reduce the tax impact of Required Minimum Distributions, manage how much of their Social Security is taxable, and potentially lower lifetime taxes.

- Roth Conversions – Timing Roth conversions during lower-income years allows retirees to shift money from tax-deferred accounts to tax-free Roth accounts at a reduced tax cost. This not only helps manage future RMDs but also creates more flexibility for drawing tax-efficient income later in retirement.

- Health Savings Accounts (HSAs) – Health Savings Accounts (HSAs) offer triple tax advantages: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. In retirement, using HSAs to cover healthcare costs can reduce the need to tap taxable accounts, helping preserve other assets and improve overall tax efficiency.

- Capital Gains Harvesting – Strategically harvesting capital gains allows retirees to realize gains in years when their income is lower, potentially keeping them in the 0% qualified investment income tax bracket. This approach helps prevent large gains from stacking on top of other income and pushing them into higher tax brackets, preserving more of their investment returns.

Maximizing Social Security Benefits with Tax Awareness

Social Security plays a central role in retirement income, but many retirees are surprised to learn that up to 85% of benefits may be subject to federal taxes, depending on their overall income. As covered in prior sections, Minnesota state allows for a complete exemption of Social Security benefits from taxable income if you stay under certain income thresholds.

Your claiming age not only affects the size of your monthly benefit but can also influence how much of it is subject to tax. Delaying benefits may give you more time to draw from other accounts strategically, reducing the taxable portion later on. Coordinating Social Security with withdrawals from tax-deferred, Roth, and taxable accounts can help manage annual income levels, keeping more of your benefits tax-free.

For married couples filing jointly, additional strategies, such as staggering when each spouse claims or balancing withdrawals across different account types, can help reduce combined tax exposure. With careful planning, you can align your claiming strategy with broader tax efficiency goals, ensuring Social Security works harder for you throughout retirement. For more support on claiming strategies for married couples, check out our past blog post.

Estate and Legacy Planning in Minnesota

When thinking about leaving a legacy, it’s important to recognize that Minnesota’s tax landscape can create unique challenges. Unlike many states, Minnesota has its own estate tax, which applies at lower exemption levels than federal rules. Coordinating both federal and state obligations is key to making sure your wealth passes smoothly to the next generation while minimizing unnecessary taxes. Some important considerations include:

- Federal vs. Minnesota estate tax – Minnesota currently imposes an estate tax with exemption levels that are significantly lower than the federal threshold ($3 ML vs. $13.99 ML), meaning more estates here may be subject to state taxes. Minnesota’s estate tax also does not allow for portability, meaning the surviving spouse is not able to use any of the deceased spouse’s unused exemption amount.

- Gifting strategies – Making gifts during your lifetime, whether to family members, charities, or through vehicles like donor-advised funds, can help reduce the taxable size of your estate and lower future estate tax liability.

- Real estate and family business succession – Passing down cabins, farmland, or family-owned businesses requires careful planning to ensure heirs can manage the transition without being burdened by estate taxes.

By proactively addressing these issues, you can create an estate plan that reflects your values, minimizes taxes, and preserves more of your legacy for the people and causes you care about most. To learn more about how Minnesota’s estate tax may impact you, read our past blog post.

Common Mistakes Near-Retirees Make with Taxes

- Coordinating Federal and State Taxes - One of the biggest pitfalls near-retirees face when it comes to tax planning is assuming that federal rules are the whole picture, while overlooking how state-specific tax laws (like those in Minnesota) can affect withdrawals.

- Planning for RMDs - Another common mistake is waiting until RMDs (Required Minimum Distributions) kick in to think about their impact, which often leads to higher-than-expected tax bills. A little planning in advance can go a long way to reducing the RMD tax hit.

- Accounting for Social Security Benefits - Many retirees also rely heavily on Social Security without realizing that a significant portion of those benefits may be taxable, depending on other income sources.

- Planning for Health Care and Long Term Care – Those who do not plan for healthcare and long-term care costs with taxes in mind may be caught off guard, especially when withdrawals from certain accounts push them into higher brackets.

Tax-Efficient Retirement Planning in Minnesota FAQs

Are Social Security benefits taxable in Minnesota?

It depends! Minnesota does allow for a full tax exemption of Social Security benefits, but you must be under certain income thresholds. You can use the table below to determine whether or not your benefits will be taxed. Note: The income values listed are for Adjusted Gross Income (AGI).

Does Minnesota have an estate tax, and how does it compare to federal rules?

Yes, Minnesota does have an estate tax, and the exemption amount for the state is much lower than for the federal estate tax. Minnesota residents are each allowed an exemption amount of up to $3 M, compared to the $13.99 ML federal exemption. Also, the Minnesota exemption amount is not portable to a surviving spouse, while the federal exemption amount is.

What is the best time to do a Roth conversion in Minnesota?

It can be a great time to consider Roth conversions when you have either fully retired or substantially reduced work income and are not yet claiming Social Security benefits. That is because your income will be at an all-time low, and you may be able to convert quite a bit of your pre-tax money into Roth money with careful planning. You can certainly consider conversions while you are claiming Social Security benefits, but be aware that this may cause you to lose some of the state exemption on taxing benefits and increase the percentage of your benefits being taxed at the federal level.

How do HSAs work for retirees living in Minnesota?

Health Savings Accounts (HSAs) are special accounts where funds can be used for qualified health care expenses and will not be taxed. These accounts can be a great way to keep your tax rate lower in retirement by using the funds for qualified expenses, along with your other sources for retirement income for non-health care expenses. You can use HSA funds to pay for Medicare premiums for parts B and D, as well as Medicare Advantage plans and any other out-of-pocket medical expenses.

Can moving to another state save on taxes in retirement?

Yes, there are certainly other states that have lower state income tax rates or that do not impose a state income tax at all. Though it is important to be aware of how to establish residency in another state if you are considering moving. Living in Minnesota does provide a great quality of life, but there is a tax cost that comes along with that benefit.

We Help Near-Retirees in Minnesota with Tax-Efficient Retirement Planning

Tax efficiency in retirement isn’t about finding one perfect strategy; it’s about weaving together federal and Minnesota-specific tax rules in a way that fits your unique situation. By coordinating where and when you draw income, and by considering strategies like Roth conversions, withdrawal sequencing, or charitable giving, you can meaningfully reduce your long-term tax costs and keep more of your retirement dollars working for you. Every retiree’s circumstances are different, which is why a personalized approach makes such a difference.

If you’d like to explore how a tax-smart strategy can be built into your retirement plan, please schedule an initial call here. Together, we can create a plan that helps you enjoy retirement with greater confidence and peace of mind.

Sources:

- https://www.revenue.state.mn.us/minnesota-income-tax-rates-and-brackets

- https://www.house.mn.gov/hrd/issinfo/sstaxes.aspx

- https://www.house.mn.gov/hrd/pubs/ss/ssmnsltx.pdf

- https://www.kiplinger.com/article/retirement/t039-c001-s003-hsas-can-reimburse-you-for-medicare-premiums-paid.html

Liz Alf

Liz Alf is the Principal of Clerestory Advisors and a fee-only CERTIFIED FINANCIAL PLANNER™ located in Minneapolis, MN. She is a member of the National Association of Personal Financial Advisors (NAPFA), the Fee Only Network, and Wealthtender. Clerestory Advisors is a fee-only financial planning firm in Bloomington, Minnesota, helping couples, independent women, and young professional families across the Twin Cities area of Minneapolis–St. Paul, prepare for retirement.