Impact of Inflation on Retirement Planning in Minnesota

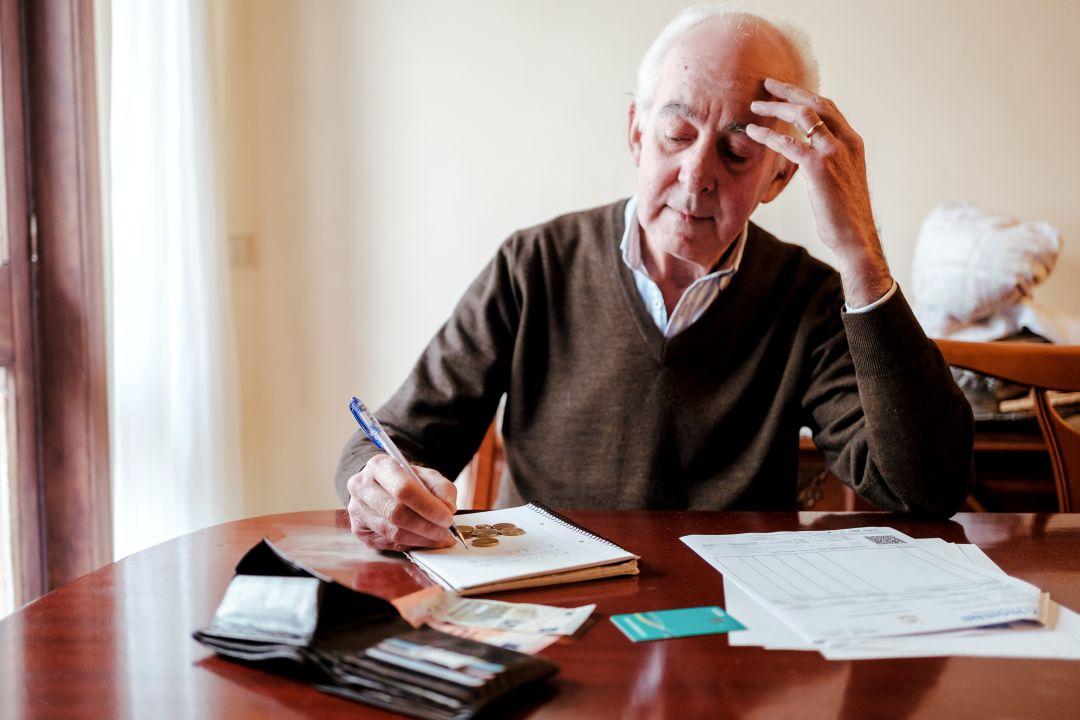

Inflation can reshape retirement plans over time. Learn how Minnesota retirees can prepare for rising costs, taxes, healthcare, and income needs.

Inflation can reshape retirement plans over time. Learn how Minnesota retirees can prepare for rising costs, taxes, healthcare, and income needs.

Learn how to financially prepare for aging in place, including home costs, healthcare, long-term care, retirement income, and family planning.

Compare long-term care insurance options in Bloomington, MN, including costs, tax benefits, and how coverage fits your retirement plan.

Should you retire in Minnesota or move away? Compare taxes, housing, healthcare, and lifestyle before making your retirement decision.

While the common house cat might not be your first pick when thinking of animals to model your investment style after, your favorite furry friend has several qualities that might be helpful to your investment outlook.

Downsizing in retirement can unlock equity, but costs, taxes, and housing choices determine how much you truly save.